By Lindsay Whitfield and Felix Maile

Most scholarship on apparel global value chains (GVCs) finds that powerful fashion brands and retailers relentlessly squeeze their suppliers in the global South. While requirements on turnaround times, quality standards and efficiency keep rising, the unit prices that suppliers receive continue to fall. Brands closely monitor suppliers’ cost structures and appropriate any efficiency gains. At the same time, they leverage fierce global competition, playing suppliers against one another by threatening to shift sourcing to lower-cost countries. As a result, apparel assembly is widely viewed as a dead end for value capture for both suppliers and workers.

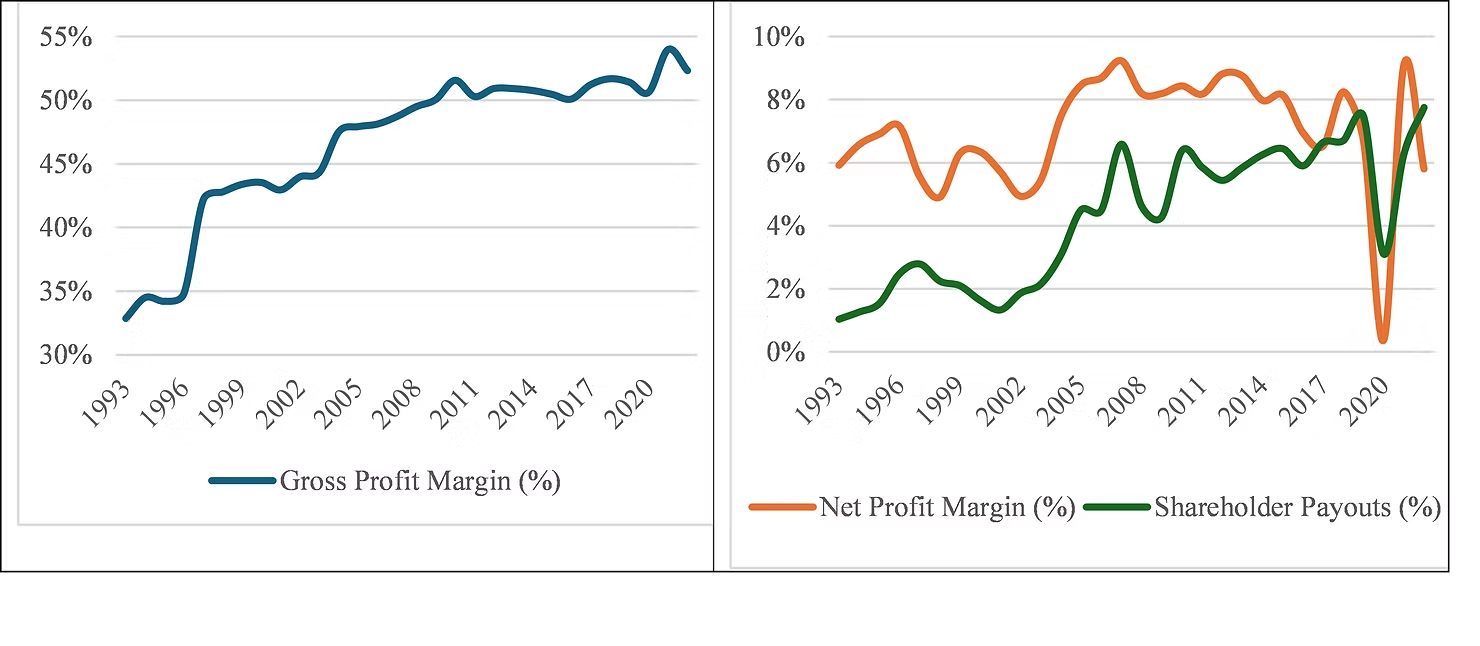

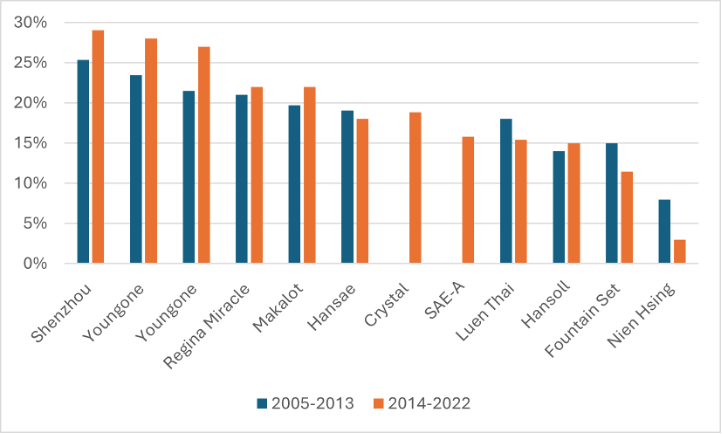

At the same time, the value capture among the largest apparel suppliers globally varies substantially: Figure 1 illustrates the gross profit margins for 12 publicly listed top apparel suppliers from the mid-2000s to the early 2020s. Three firms in particular – Shenzhou, Eclat, and Youngone – stand far above the rest. Not only do they consistently achieve substantially higher margins than their competitors, but since the 2010s their profitability has continued to climb, even as margins for most other suppliers have stagnated or declined. This creates an empirical puzzle: how do some apparel suppliers manage to escape the “supplier squeeze”?

Figure 1. Annual gross profit margin (%) of giant apparel suppliers, 2005-2022

We solve this puzzle in a new article on ‘Rethinking economic upgrading in apparel GVCs: Value capture through strategic partnerships in product innovation cycles’. The article traces how ‘giant apparel contract manufacturers’ from Hong Kong, South Korea, Taiwan, Sri Lanka, and China have sought to capture more value over the past 25 years. It shows that even among the largest suppliers globally, only few suppliers have been able to extract concession on profit sharing from fashion brands and retailers. They do so by entering strategic partnerships with lead firms operating within what we call product innovation cycles.

Product innovation cycles are time-specific end-market dynamics in which lead firms temporarily escape competition with other lead firms by pioneering new products characterized by rapid growth and higher profit margins. To commercialize these products, fashion brands and retailers require suppliers with specialized manufacturing capabilities. Entering such strategic partnerships requires building specialized complementary assets such as advanced synthetic fabric capabilities. Strategic partnerships tend to be short-lived. They end once the lead firms (or the suppliers themselves) are emulated by competitors with the same capabilities. Thus, economic upgrading (understood as capturing more value along the chain) is only a transient condition that must be continuously renewed through new strategic partnerships.

Felix Maile is a doctoral researcher in development economics at the University of Vienna.

Lindsay Whitfield is Professor for Business and Development at Copenhagen Business School.

Read more in our new Blog Post and in our new open access paper ‘Rethinking economic upgrading in apparel GVCs: Value capture through strategic partnerships in product innovation cycles’.